Aseem Bordia: Paper traders review the situation as mill yields and price rise

It is not a mere coincidence that some paper manufacturers have been increasing prices. Concurrently, some paper mill associations have been crying hoarse and seeking protection, level playing field, imposition of countervailing duties, safeguard and anti-dumping duties, imposition of quality control measures and quality control orders and even going to the extent of seeking a ban on imports of paper and paperboards by giving statistics about the imports and exports of paper and paperboards.

16 Oct 2023 | By PrintWeek Team

The paper mills claim to be Atma Nirbhar and Make in India. However the facts prove otherwise, even after 75 years of independence.

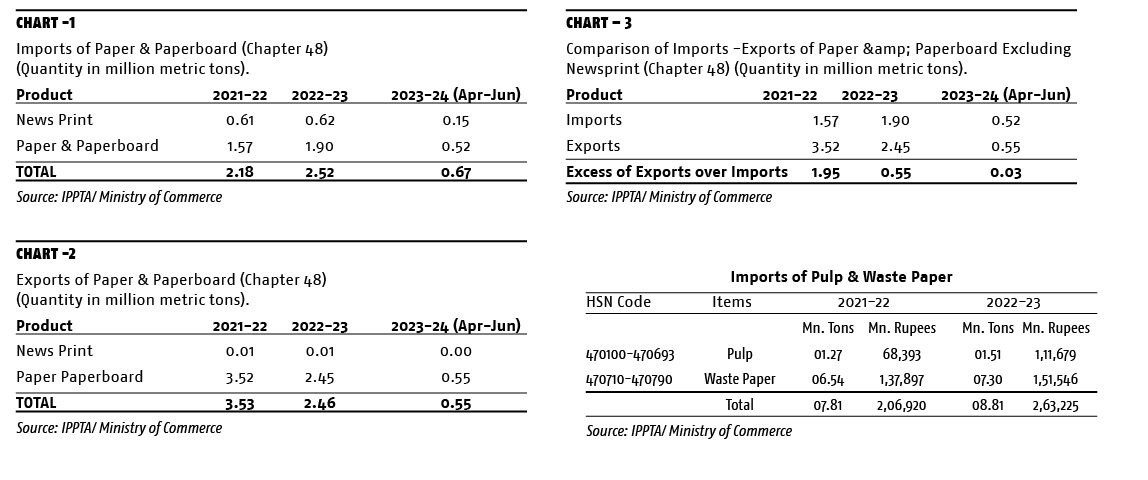

The true comparison of imports and exports of paper and paperboards excluding newsprint (being under Newsprint Control Order (NCO) 2004) is given below:

Thus, it is very clear that the exports of paper and paperboards have been higher in FY 21-22, FY 22-23 and even in the first quarter of FY 23-24.

Also, it may be noted that paper can be recycled 5-7 times. Every ton of finished paper imported into the country provides 5-7 times fibre for remaking of paper. This saves the foreign exchange on imports of waste paper. However, in the case of exports, every ton of export of finished paper, indirectly exports 5-7 tons of fibre also. The country has to thus make a higher foreign exchange payout for importing 5-7 tons of waste paper in lieu of every tons of exports of finished paper.

According to the DPIIT Annual Report of 2022-23, the share of wood, agro and waste paper-based mills stand at 18%, 7% and 75% respectively in the total production. The IPMA website displays a 38% recovery rate for waste paper as against 68% in the US and 71.4% in Europe. The recycling rate for cardboard boxes was 93% in the US.

The precious foreign exchange spent on imports of pulp and waste paper is given above. Meanwhile the paper industry talks about being Atma Nirbhar and Make in India.

The real story of prices begins in the Covid period. Price increases by the manufacturers were at sweet will, some were doing it daily, some doing on minute-to-minute basis by sending messages on WhatsApp, pending and confirmed orders were not fulfilled, cancelled and or put on hold. This placed the entire trade and the user/ consumer in a difficult and painful situation.

There being no restrictions, the prices of paper and paperboards breached all levels and attained a record peak. The manufacturers were enjoying the situation and reaped windfall profits. The exports overtook imports in FY 2020-21 for the first-time.

The beginning of the new financial year brought with it a change much to the disliking of the domestic paper manufacturers. They were already facing some pressures because of the resistance to the high levels of prices by the user and consumer sector.

In April 2023, the Shanghai Pulp Week was hosted in Shanghai, China. Pulp manufacturers from around the world over present were eager to negotiate prices and offered discounts. The Chinese buyers played a smart game and offered low prices. This resulted in discounts going up. Ultimately by the end of the event no transpired and the weakness in pulp prices was evident to one and all. During the next few days, the inevitable happened, the pulp prices crashed and hardwood pulp breached even USD 500. Indian paper manufacturers took the benefit of low pulp prices entered into contracts for substantial quantities.

The waste paper market crashed and the domestic paper manufacturers leveraged the low prices.

The crash in pulp prices and waste paper prices started a chain reaction in global markets and especially in China. The export order book of Indian players, especially for the brown grades and boards started to clean up with no fresh orders. The inventories started piling up as the demand in the domestic market was also at low level.

The prices of paper and paperboards started to tumble down.

Again, this started a new cycle of cancellation of orders, refusal to accept deliveries and all sorts of other trade issues. The manufacturers were compelling the traders to accept more supplies than the normal levels. All this led to very high inventory levels at the trade and user levels. Further, the trade and user community were suffering because of earlier high-priced inventories making them reluctant to place new orders as they were facing huge losses. In all, the situation in the trade was very bleak.

The situation in some of the paper consuming sectors such as diaries, calendars, notebooks, examination papers, office papers seem to be in a negative phase. Even the packaging sector has started to reduce packaging and or seeking alternatives. The high hopes about the National Education Policy (NEP) creating additional demand has not materialised. The green shoots are not yet visible.

The international market for pulp, paper and paperboard and waste paper seems to be in a status quo for the remaining period of calendar year 2023. Some of the leading paper manufacturers have come with statements of no changes in prices till the end of 2023. Pulp and waste paper prices are soft. Additional new pulp capacities in South America are expected to come live. The collection and recycling rates for waste paper in Europe and the United States, two major markets, are going up. Prices of waste paper too are soft. A record additional capacity for paperboard is expected to start in the next two years in Asia. There is every possibility of demand supply mismatch in this region.

The domestic paper manufacturers have a tendency in creating a narrative by announcing price increases to work on the sentiments of the trade and user to keep their order books healthy, but having no logic and or reason to justify the same.

In India, the paper trade is carrying huge inventory and much of it is high priced with losses written all over. The user and or consumer high priced inventories. The trade and users do not have high hopes for additional demands in the festive season. They are also reluctant in increasing their inventories, on the contrary they are trying to reduce the same. The sentiments are weak.

Lastly, in the present scenario, it is advisable not to accept the announcements of the paper manufacturers at the face value, but to take it with a pinch of salt.

Aseem Bordia is president of Federation Of Paper Traders' Associations Of India

See All

See All